Finance

This section of the Annual Report contains information about our financial performance.

For more details and archives of financial information please see the links below:

Value for money

Great Places is committed to ensuring that it delivers Value for Money (VfM) services for its customers, communities and other stakeholders. This touches on every aspect of the services that Great Places delivers, so making sure that customers receive, understand and influence our decision-making processes is paramount in our approach. Achieving Value for Money is a fundamental part of sound business practice as well as being a regulatory requirement and we are committed to finding the right balance between quality, cost and customer need.

To ensure that we achieve Value for Money, Great Places’ Board approved a new Value for Money strategy in October 2021. The strategy details the actions we will take to ensure that Great Places continues to deliver value for money for our customers, and that we make the right spending decisions for the right reasons.

The objective of the VfM strategy is to ensure that we meet the needs of our customers and deliver our Corporate Plan objectives in the most economic, efficient and effective way. To do this we have adopted five strategic goals which are:

- Creating and embedding a ‘spend it like your own’ ethos;

- Valuing our customers;

- Making the right decisions for the right reasons;

- Business Brain, Social Heart;

- Communicate, Evidence and Learn.

A detailed action plan has been developed to support the delivery of the strategy with oversight of delivery provided by the Great Value Group.

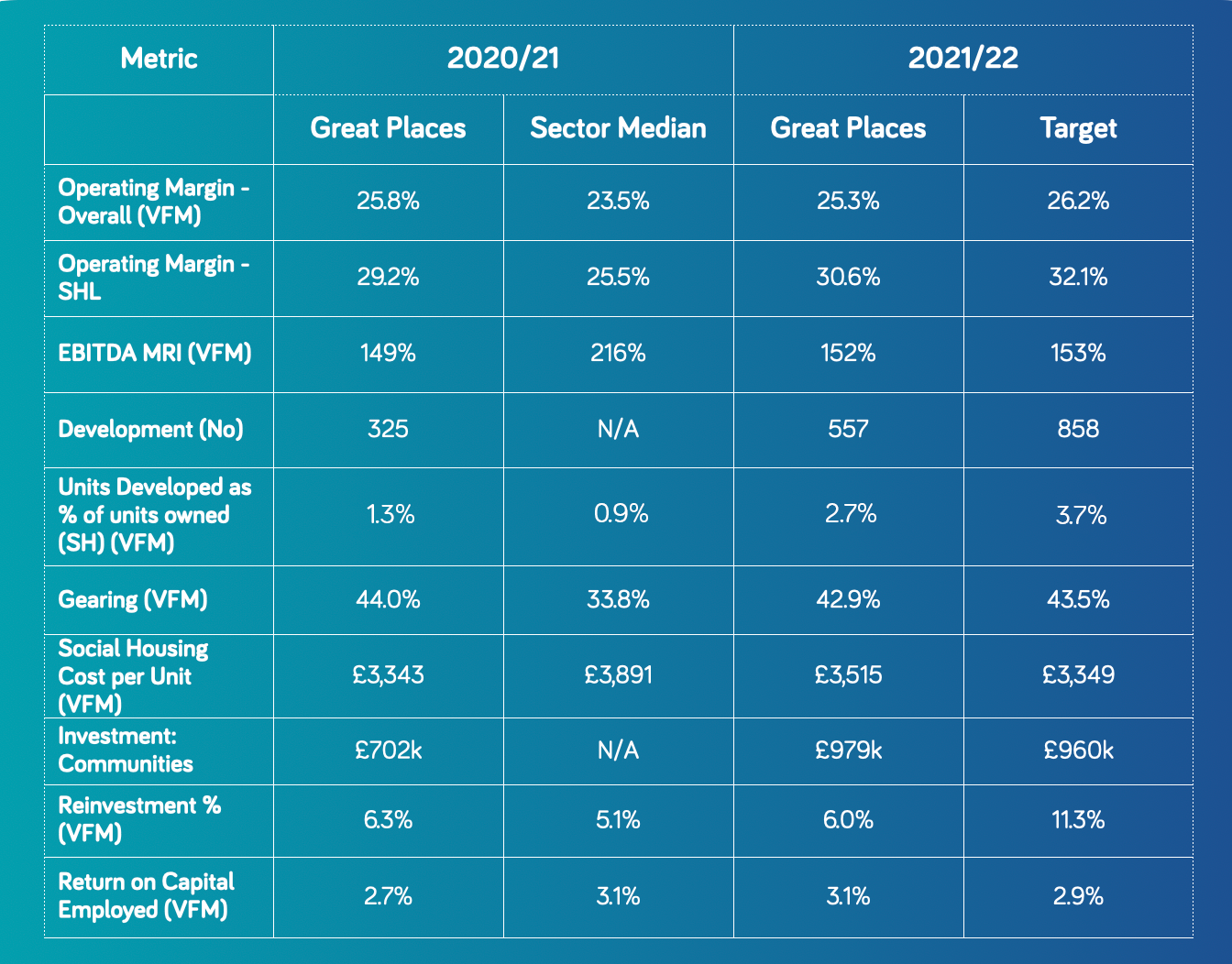

Value for Money metrics

Our overall operating margin (the proportion of surplus generated from turnover on a provider’s day-to-day activities) is at 25.3%; this is better than the sector median in previous years and in line with our target. Our overall operating margin for 2021/22 has decreased slightly from 2020/21 performance. Our operating margin for social housing lettings is 30.6%, and has improved on the prior year, which was already outperforming the sector median.

Earnings before interest, tax, depreciation and amortisation with major repairs included (EBITDA MRI) is designed to show what cash the organisation generates from day-to-day activities. Our performance in this area remains strong and has improved on the previous year, remaining in line with our target. This should be viewed in line with our gearing performance which shows how dependent we are on lending when this is compared to the assets the Group holds. As shown in the table below, we have seen this improve to achieve our target for the year (due in part to the increase in the number of properties developed this year), which comfortably exceeded the 2020/21 figure.

Financial Resilience

Being a bigger and stronger business since the merger significantly enhances our financial resilience.

Despite challenges such as a volatile political and economic environment, shortages of skilled labour and inflationary cost increases Great Places has continued to see some fantastic achievements in the last 12 months.

In 2021/22 we generated a surplus of £21M and delivered a strong performance across a number of key financial metrics. Our long-term financial plan demonstrates that the organisation is financially sound and able to withstand challenges that present themselves. We have a strong liquidity position and are well funded for our future development programme.

As we look to the future, our governance and financial viability ratings of G1 V1 gives us the assurance that we are managing our risks effectively, despite the ongoing and challenging operating conditions. We remain confident that we have strong governance, financial management, strategic business planning and stress testing arrangements in place.

Our Credit ratings with Moody’s and Fitch remain unchanged (A3 stable and A+) and demonstrate that we remain in a strong position to continue to effectively manage the risks facing our business moving forward.

Additional liquidity

The Group remains in a very strong position to meet our funding needs for at least the next two years. The renegotiated and restructured £100m revolving credit facility with RBS/Natwest completed in March 2022, combining legacy Great Places and Equity Housing Group debt, increasing the facility from £85m to £100m and extending its maturity to 2027.